As filed with the Securities and Exchange Commission on June 26, 2002

Registration No. 333-87044

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

RED ROBIN GOURMET BURGERS, INC.

(Exact name of registrant as specified in its charter)

| Delaware |

|

5812 |

|

84-1573084 |

| (State or other jurisdiction of

incorporation or organization) |

|

(Primary standard industrial

classification code number) |

|

(I.R.S. employer

identification number) |

5575 DTC Parkway, Suite 110

Greenwood Village, Colorado 80111

(303) 846-6000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Michael J. Snyder

Chief Executive Officer

5575 DTC Parkway, Suite 110

Greenwood Village, Colorado 80111

(303) 846-6000

(Name, address, including zip code, and telephone number, including area code,

of agent for service)

Copies To:

| Thomas J. Leary Brandi R.

Steege O’Melveny & Myers LLP 610 Newport Center

Drive, Suite 1700 Newport Beach, California 92660 (949)

760-9600 |

|

Valerie Ford Jacob Stuart H.

Gelfond Fried, Frank, Harris, Shriver & Jacobson One New

York Plaza New York, New York 10004 (212)

859-8000 |

Approximate date of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended

(the “Securities Act”) check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities

Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to

Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus

is expected to be made pursuant to Rule 434, check the following box. ¨

The registrant hereby amends this registration

statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with

Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. Red Robin may not sell these securities until the registration statement

filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and Red Robin is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED JUNE 26, 2002

PROSPECTUS

5,038,000 Shares

Common Stock

Red Robin Gourmet Burgers, Inc. and the selling stockholders are offering shares of common stock in

a firmly underwritten offering. This is Red Robin’s initial public offering, and no public market currently exists for our shares. Red Robin anticipates that the initial public offering price for its shares will be between $14.00 and

$16.00 per share. Red Robin will not receive any of the proceeds from shares sold by the selling stockholders.

Our common stock has been approved for quotation on The Nasdaq Stock Market’s National Market under the symbol “RRGB.”

Investing in our common stock involves risks that are

described under “Risk Factors” beginning on page 7 of this prospectus.

| |

|

Per Share |

|

Total |

|

|

|

|

|

| Offering Price |

|

$ |

|

|

$ |

|

| Discounts and Commissions to Underwriters |

|

$ |

|

|

$ |

|

| Offering Proceeds to Red Robin |

|

$ |

|

|

$ |

|

| Offering Proceeds to the Selling Stockholders |

|

$ |

|

|

$ |

|

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or has determined if this prospectus is truthful or complete. Any representation to the

contrary is a criminal offense.

Some of the selling stockholders have granted the underwriters the right to

purchase up to an additional 755,700 shares of common stock to cover any over-allotments. The underwriters can exercise this right at any time from time to time within 30 days after the offering. Delivery of the shares of common stock will be

made on or about , 2002.

| Banc of America Securities LLC |

|

U.S. Bancorp Piper Jaffray |

Wachovia Securities

The date of this prospectus is

, 2002

| |

|

Page

|

| |

|

i |

| |

|

1 |

| |

|

7 |

| |

|

16 |

| |

|

17 |

| |

|

18 |

| |

|

19 |

| |

|

20 |

| |

|

21 |

| |

|

23 |

| |

|

38 |

| |

|

51 |

| |

|

65 |

| |

|

69 |

| |

|

72 |

| |

|

74 |

| |

|

76 |

| |

|

80 |

| |

|

83 |

| |

|

83 |

| |

|

83 |

| |

|

F-1 |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information that is different. We are offering to sell and seeking offers to buy shares of our common

stock only in jurisdictions where offers or sales are permitted. The information in this document may only be accurate on the date of this document. Our business, financial condition or results of operations may have changed since that date.

Red Robin®, America’s Gourmet Burgers & Spirits® and Mad Mixology® are federally registered trademarks and service marks owned by Red Robin. Red Robin® is also registered in Canada. This prospectus also contains trademarks of companies other than Red Robin and use of such marks in this prospectus does not indicate an affiliation with or endorsement by such third parties.

Throughout this prospectus, our fiscal years

ended December 28, 1997, December 27, 1998, December 26, 1999, December 31, 2000 and December 30, 2001 are referred to as years 1997, 1998, 1999, 2000 and 2001, respectively. Our fiscal year consists of 52 or 53 weeks and ends on the last Sunday in

December in each fiscal year. Fiscal year 2000 included 53 weeks. All other fiscal years shown included 52 weeks. In 2001, our first quarter ended on April 22, 2001 and is referred to throughout this prospectus as first quarter 2001 and in 2002, our

first quarter ended on April 21, 2002 and is referred to throughout this prospectus as first quarter 2002. Our first quarters include 16 weeks and our second, third and fourth quarters each include 12 weeks.

Unless we indicate otherwise, all of the information in this prospectus assumes:

| |

• |

|

the underwriters will not exercise their over-allotment option to purchase up to 755,700 additional shares of our common stock from some of the selling

stockholders at the price set forth on the cover of this prospectus; |

| |

• |

|

an initial offering price of $15.00 per share, the midpoint of the range set forth on the cover of this prospectus; |

| |

• |

|

no exercise of options to purchase an aggregate of 504,466 shares of common stock which were outstanding as of May 19, 2002 under our stock option plans; and

|

| |

• |

|

that we have completed a one-for-2.9 reverse stock split that we intend to complete prior to the consummation of this offering.

|

i

This summary highlights information contained elsewhere in this

prospectus. This summary is not complete and does not contain all of the information you should consider before investing in our common stock. You should read the entire prospectus carefully, including the “Risk Factors” section and our

consolidated financial statements and the related notes. References in this prospectus to “Red Robin,” “company,” “we,” “us” and “our” refer to the business of Red Robin Gourmet Burgers, Inc. and its

subsidiaries.

OUR BUSINESS

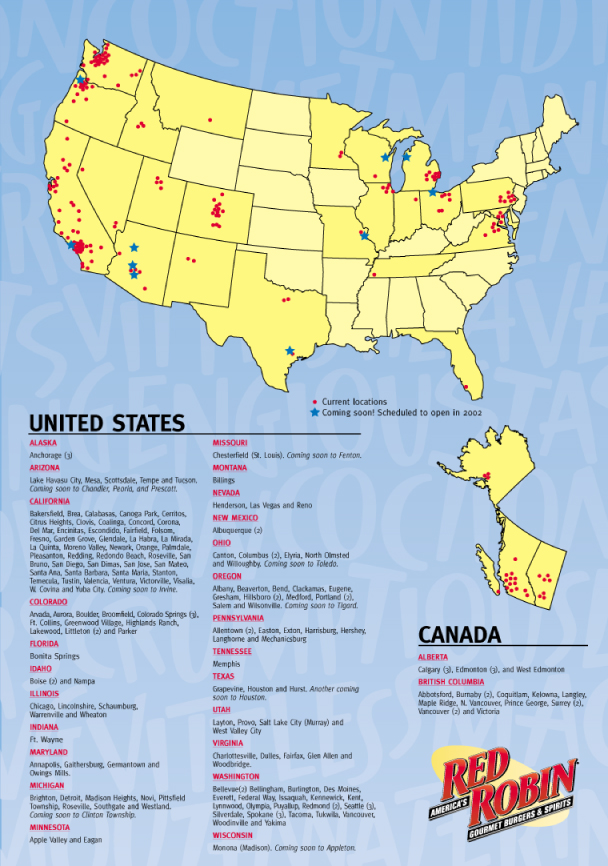

Red Robin is a casual dining restaurant chain focused on serving an imaginative selection of high quality gourmet burgers in a family-friendly atmosphere. We currently own and operate 90 restaurants in

12 states, and have 99 additional restaurants operating under franchise or license agreements in 19 states and Canada.

Our menu is centered around our signature product, the gourmet burger, which we make from beef, chicken, veggie, fish, turkey and pot roast and serve in a variety of recipes. We offer a wide selection of toppings for our gourmet

burgers, including fresh guacamole, roasted green chilies, honey mustard dressing, grilled pineapple, crispy onion straws, sautéed mushrooms and a choice of six different cheeses. In addition to our gourmet burgers, which accounted for

approximately 44.0% of our total food sales in 2001, we also serve an array of other food items that are designed to appeal to a broad group of guests, including salads, soups, appetizers, other entrees such as rice bowls and pasta, desserts and our

signature Mad Mixology® alcoholic and non-alcoholic specialty beverages.

Our restaurants are designed to

create a fun and memorable dining experience in a family-friendly atmosphere and provide our guests with an exceptional dining value. Our concept attracts a broad guest base by appealing to the entire family.

OUR CONCEPT AND BUSINESS STRATEGY

Our objective is to be the leading gourmet burger and casual dining restaurant destination. To achieve our objective, we have developed the following strategies.

| |

• |

|

Focus on our key guiding principals, or “cornerstones,” that drive our success. Values, people, burgers and time.

|

| |

• |

|

Offer high quality, imaginative menu items. Our restaurants feature imaginative menu items that showcase recipes and capture

tastes and flavors that our guests do not typically associate with burgers, salads and sandwiches. |

| |

• |

|

Create a fun, festive and memorable dining experience. We promote an exciting, high-energy and family-friendly atmosphere by

decorating our restaurant interiors with an eclectic selection of celebrity posters, three-dimensional artwork, carousel horses and statues of our mascot “Red”. |

| |

• |

|

Provide an exceptional dining value with broad consumer appeal. We offer generous portions of high quality, imaginative food and

beverages for a per person average check of approximately $10.00, which we believe differentiates us from many of our competitors who have significantly higher average guest checks. |

| |

• |

|

Deliver strong unit economics. Our comparable company-owned restaurants generated average sales of approximately $3.0 million and

restaurant-level operating profit of approximately $618,000, or 20.5% of comparable company-owned restaurant sales in 2001. The average cash investment cost for

|

1

our free-standing restaurants opened in 2001 was approximately $1.7 million, excluding pre-opening costs and land. Our comparable company-owned restaurants generated average sales of

approximately $2.9 million and restaurant-level operating profit of approximately $533,000, or 18.4% of comparable company-owned restaurant sales in 2000. The average cash investment cost for our free-standing restaurants opened in 2000 was

approximately $1.8 million, excluding pre-opening costs and land.

| |

• |

|

Pursue disciplined restaurant and franchise growth. Our disciplined expansion strategy includes both company-owned and franchised

development. In 2002, we have opened four new company-owned restaurants, expect to open six additional new company-owned restaurants and relocate one restaurant. Our franchisees have opened four new restaurants and we expect them to open three

additional restaurants this year. |

| |

• |

|

Build awareness of the Red Robin® America’s Gourmet Burgers & Spirits® brand. We believe we have become well

known within our markets for our signature menu items and we intend to strengthen this brand loyalty by continuing to offer new menu items and deliver a consistently memorable guest experience. |

| |

• |

|

Continue to capitalize on favorable lifestyle and demographic trends. We believe we have benefited from several key trends that

have helped drive our business. These trends include the expected increase in consumption of food away from home and the large and growing teen population. |

OUR GROWTH STRATEGIES

We believe that there are

significant opportunities to grow our concept and brand on a nationwide basis through both new company-owned and franchised restaurants. We believe that our concept and brand can support as many as 850 additional company-owned or franchised

restaurants throughout the United States.

Company-owned restaurants. Our primary

source of expansion and growth in the near term will be the addition of new company-owned restaurants. We are pursuing a disciplined growth strategy and intend to develop many of our new restaurants in our existing markets, and selectively enter

into new markets. Our growth strategy incorporates a cluster strategy for market penetration, which we believe will enable us to gain operating efficiencies, increase brand awareness and enhance convenience and ease of access for our guests, all of

which we believe will lead to significant repeat business. Our site selection criteria for new restaurants is flexible and allows us to adapt to a variety of locations near high activity areas such as retail centers, big box shopping centers and

entertainment centers.

Franchised Restaurants. The other key aspect of our

growth strategy is the continued development of our franchise restaurants. We expect the majority of our new franchise restaurant growth to occur through the development of new restaurants by new franchisees, primarily in the Northeast, Midwest and

the South. We intend to continue to strengthen our franchise system by attracting experienced and well-capitalized area developers who are quality-conscious restaurant operators and who possess the expertise and resources to execute the development

of new restaurants on a large scale.

OUR HISTORY

Red Robin opened its first restaurant in 1969, in Seattle, Washington near the University of Washington campus. In 1996, Mike Snyder, then our leading franchisee, became

our president and implemented a number of strategic initiatives, including strengthening our gourmet burger concept, recruiting a new management team, upgrading management information systems, streamlining operations and improving guest service. As

a result of these and other initiatives, we increased the average annual restaurant sales of our comparable company-owned

2

restaurants from $2.1 million in 1995 to $3.0 million in 2001 and expanded comparable restaurant-level operating profit margins from 15.8% in 1995 to 20.5% in 2001. In 2000, we completed a

recapitalization of our company, and acquired Mike Snyder’s 14-unit franchise company, The Snyder Group Company. In addition, Quad-C, a private equity firm whose principals have substantial restaurant experience, made an equity investment of

$25.0 million in our company through its affiliates.

RISK FACTORS

An investment in our common stock involves a high degree of risk. The following risks, as well as the risks discussed in “Risk Factors,” should be carefully

considered before investing in our common stock:

| |

• |

|

our ability to open new restaurants, secure sufficient new space and manage our planned expansion; |

| |

• |

|

the continued service of key management personnel; |

| |

• |

|

changes in consumer preferences or consumer discretionary spending; |

| |

• |

|

health concerns regarding beef or other food products; |

| |

• |

|

the effect of competition in the restaurant industry; |

| |

• |

|

the ability of our franchisees to take actions that could harm our business; |

| |

• |

|

adverse economic and other developments in the Western United States where 83.3% of our company-owned restaurants are located; and

|

| |

• |

|

Quad-C, Skylark Co., Ltd., Mike Snyder and our other officers, directors and principal stockholders will hold approximately 58.0% of our common stock after this

offering and, acting individually or together, will be able to exert significant influence over all matters requiring stockholder approval, including the election of directors and significant business transactions. |

Our principal executive offices are

located at 5575 DTC Parkway, Suite 110, Greenwood Village, Colorado 80111. Our telephone number is (303) 846-6000. Our website is www.redrobin.com. The information on our website is not part of this prospectus.

3

THE OFFERING

| Common stock offered by: |

|

|

| |

| Red Robin Gourmet Burgers, Inc. |

|

4,000,000 shares |

| Selling stockholders |

|

1,038,000 shares |

| |

| Common stock to be outstanding after this offering |

|

15,025,654 shares |

| |

| Use of proceeds |

|

We intend to use the proceeds of this offering: |

| |

| |

|

• to repay approximately $47.9 million of indebtedness under our term loan,

including related fees; |

| |

| |

|

• to repay approximately $3.5 million of indebtedness under our revolving

credit facility; and |

| |

| |

|

• to repay approximately $2.1 million of indebtedness under one real estate

and three equipment loans, including related fees. |

| |

| |

|

The remaining net proceeds will be used for general corporate purposes, which may include the opening of new restaurants or the acquisition of existing

restaurants from franchisees if we receive sufficient proceeds. We will not receive any of the proceeds from the sale of shares by the selling stockholders. See “Use of Proceeds.” |

| |

| Proposed Nasdaq National Market symbol |

|

RRGB |

The number of shares of common stock to be outstanding after

this offering is based on our shares outstanding as of May 19, 2002. This information excludes:

| |

• |

|

1,475,690 shares of common stock reserved for issuance under our stock option plans, of which 504,466 shares are subject to options outstanding at a weighted

average exercise price of $5.83 per share; and |

| |

• |

|

300,000 shares of common stock reserved for issuance under our employee stock purchase plan. |

4

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING DATA

| |

|

Fiscal Year Ended

|

|

|

First Quarter Ended

|

|

| |

|

1999

|

|

|

2000(1)

|

|

|

2001

|

|

|

2001

|

|

|

2002

|

|

| |

|

(in thousands, except per share data, restaurant-related data and footnotes) |

|

| Statement of Income Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

(unaudited) |

| Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Restaurant |

|

$ |

121,430 |

|

|

$ |

180,413 |

|

|

$ |

214,963 |

|

|

$ |

64,572 |

|

|

$ |

76,317 |

|

| Franchise royalties and fees |

|

|

8,249 |

|

|

|

8,247 |

|

|

|

9,002 |

|

|

|

2,822 |

|

|

|

2,757 |

|

| Rent revenue |

|

|

333 |

|

|

|

510 |

|

|

|

520 |

|

|

|

120 |

|

|

|

127 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total revenues |

|

|

130,012 |

|

|

|

189,170 |

|

|

|

224,485 |

|

|

|

67,514 |

|

|

|

79,201 |

|

| Income from operations |

|

|

7,145 |

|

|

|

8,805 |

|

|

|

18,740 |

|

|

|

5,127 |

|

|

|

5,993 |

|

| Interest expense |

|

|

4,156 |

|

|

|

6,482 |

|

|

|

7,850 |

|

|

|

2,500 |

|

|

|

2,217 |

|

| Interest income |

|

|

(186 |

) |

|

|

(742 |

) |

|

|

(746 |

) |

|

|

(208 |

) |

|

|

(100 |

) |

| Other expense |

|

|

391 |

|

|

|

191 |

|

|

|

190 |

|

|

|

63 |

|

|

|

25 |

|

| (Provision) benefit for income taxes(2) |

|

|

1,596 |

|

|

|

12,557 |

|

|

|

(3,722 |

) |

|

|

(901 |

) |

|

|

(1,374 |

) |

| Net income(2) |

|

|

4,380 |

|

|

|

15,431 |

|

|

|

7,724 |

|

|

|

1,871 |

|

|

|

2,476 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income per common share(2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

$ |

1.47 |

|

|

$ |

2.07 |

|

|

$ |

0.77 |

|

|

$ |

0.19 |

|

|

$ |

0.25 |

|

| Diluted |

|

$ |

1.47 |

|

|

$ |

2.07 |

|

|

$ |

0.75 |

|

|

$ |

0.18 |

|

|

$ |

0.23 |

|

| Shares used in computing net income per common share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

|

2,971 |

|

|

|

7,444 |

|

|

|

10,085 |

|

|

|

10,076 |

|

|

|

10,090 |

|

| Diluted |

|

|

2,971 |

|

|

|

7,444 |

|

|

|

10,236 |

|

|

|

10,170 |

|

|

|

10,650 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Selected Operating Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| System-wide restaurants open at end of period |

|

|

144 |

|

|

|

164 |

|

|

|

182 |

|

|

|

165 |

|

|

|

186 |

|

| Company-owned restaurants open at end of period |

|

|

46 |

|

|

|

73 |

|

|

|

77 |

|

|

|

72 |

|

|

|

88 |

|

| Average annual comparable company-owned restaurant sales(3) |

|

$ |

2,664 |

|

|

$ |

2,890 |

|

|

$ |

3,020 |

|

|

|

|

|

|

|

|

|

| Comparable company-owned restaurant sales increase(3) |

|

|

5.8 |

% |

|

|

6.9 |

% |

|

|

2.0 |

% |

|

|

2.6 |

% |

|

|

0.4 |

% |

| Restaurant-level operating profit(4) |

|

$ |

20,340 |

|

|

$ |

32,423 |

|

|

$ |

41,215 |

|

|

$ |

11,497 |

|

|

$ |

14,298 |

|

| EBITDA(5) |

|

|

12,539 |

|

|

|

16,870 |

|

|

|

29,231 |

|

|

|

8,279 |

|

|

|

9,592 |

|

| EBITDA margin(5) |

|

|

9.6 |

% |

|

|

8.9 |

% |

|

|

13.0 |

% |

|

|

12.3 |

% |

|

|

12.1 |

% |

| |

|

April 21, 2002

|

| |

|

Actual

|

|

As Adjusted(6)

|

| |

|

(unaudited) |

| Balance Sheet Data: |

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

6,547 |

|

$ |

10,695 |

| Total assets |

|

|

154,188 |

|

|

156,168 |

| Long-term debt, including current portion |

|

|

78,743 |

|

|

30,122 |

| Total stockholders’ equity |

|

|

49,475 |

|

|

100,076 |

(1) |

|

In May 2000, we purchased all of the outstanding capital stock of one of our franchisees, The Snyder Group Company, for approximately $23.7 million plus

liabilities assumed of $20.0 million, thereby acquiring 14 restaurants and significantly changing our capital structure. See the financial statements of The Snyder Group Company and the related notes included elsewhere in this prospectus.

|

|

|

In addition, in May 2000, we sold 4,310,344 shares of our common stock to affiliates of Quad-C, a private equity firm, for $25.0 million. The proceeds were used

to pay off debentures and promissory notes, as well as pay down bank debt and fund new restaurant construction. |

5

(2) |

|

Net income in 1999 included a benefit for income taxes of $1.6 million and net income in 2000 included a benefit for income taxes of $12.6 million, in each case

as a result of the reversal of previously recorded deferred tax asset valuation allowance. Due to our improved profitability, the deferred tax asset valuation allowance was reversed because it became more likely than not that the deferred tax asset

would be realized in the future. |

(3) |

|

Company-owned restaurants become comparable in the first period following the first full fiscal year of operations. For example, the restaurants we acquired in

May 2000 from The Snyder Group Company are included in comparable company-owned restaurants in 2002. |

(4) |

|

We define restaurant-level operating profit to be restaurant sales minus restaurant operating costs, excluding restaurant closures and impairment costs. It does

not include general and administrative costs, depreciation and amortization, franchise development costs and pre-opening costs. Although restaurant-level operating profit is a measure commonly used in the restaurant industry to evaluate operating

performance, it is not a measurement determined in accordance with generally accepted accounting principles and should not be considered in isolation or as an alternative to net income, cash flows generated by operations, investing or financing

activities or other financial statement data presented as indicators of financial performance or liquidity. Restaurant-level operating profit as presented may not be comparable to other similarly titled measures of other companies. The following

table sets forth our calculation of restaurant-level operating profit: |

| |

|

|

|

|

|

|

|

First Quarter Ended

|

| |

|

1999

|

|

2000

|

|

2001

|

|

2001

|

|

2002

|

| |

|

(in thousands) |

|

(unaudited) |

| Restaurant revenue |

|

$ |

121,430 |

|

$ |

180,413 |

|

$ |

214,963 |

|

$ |

64,572 |

|

$ |

76,317 |

| Cost of sales |

|

|

30,159 |

|

|

43,945 |

|

|

50,914 |

|

|

15,952 |

|

|

17,897 |

| Labor |

|

|

43,504 |

|

|

64,566 |

|

|

74,854 |

|

|

22,639 |

|

|

27,428 |

| Operating |

|

|

19,429 |

|

|

27,960 |

|

|

33,195 |

|

|

10,317 |

|

|

11,412 |

| Occupancy |

|

|

7,998 |

|

|

11,519 |

|

|

14,785 |

|

|

4,167 |

|

|

5,282 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Restaurant-level operating profit |

|

$ |

20,340 |

|

$ |

32,423 |

|

$ |

41,215 |

|

$ |

11,497 |

|

$ |

14,298 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(5) |

|

EBITDA represents earnings before interest, taxes, depreciation and amortization. EBITDA is another measure commonly used to evaluate operating performance.

EBITDA is not a measurement determined in accordance with generally accepted accounting principles and should not be considered in isolation or as an alternative to net income, cash flows generated by operations, investing or financing activities or

other financial statement data presented as indicators of financial performance or liquidity. EBITDA as presented may not be comparable to other similarly titled measures of other companies. EBITDA margin is calculated as EBITDA divided by total

revenues. The following table sets forth our calculation of EBITDA: |

| |

|

|

|

|

|

|

|

First Quarter Ended

|

| |

|

1999

|

|

2000

|

|

2001

|

|

2001

|

|

2002

|

| |

|

(in thousands) |

|

(unaudited) |

| Income from operations |

|

$ |

7,145 |

|

$ |

8,805 |

|

$ |

18,740 |

|

$ |

5,127 |

|

$ |

5,993 |

| Depreciation and amortization |

|

|

5,394 |

|

|

8,065 |

|

|

10,491 |

|

|

3,152 |

|

|

3,599 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| EBITDA |

|

$ |

12,539 |

|

$ |

16,870 |

|

$ |

29,231 |

|

$ |

8,279 |

|

$ |

9,592 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(6) |

|

As adjusted information gives effect to the application of the net proceeds from the sale of 4,000,000 shares of our common stock offered by us in this offering

at an initial offering price of $15.00 per share, less the underwriting discount and estimated offering expenses payable by us, and the use of the proceeds from this offering to repay approximately $47.9 million of indebtedness under our term loan,

including related fees, approximately $3.5 million of indebtedness under our revolving credit facility and approximately $2.1 million of indebtedness under one real estate and three equipment loans, including related fees. This information also

reflects the non-cash charge to earnings of approximately $2.2 million from the write-off of deferred loan fees and the cash charge of approximately $1.9 million from pre-payment penalty fees related to the repayment of the indebtedness noted above.

|

6

An investment in our common stock involves a high degree of risk. You

should carefully read and consider the risks described below before deciding to invest in our common stock. If any of the following risks actually occurs, our business, financial condition, results of operation or cash flows could be materially

harmed. In any such case, the trading price of our common stock could decline, and you could lose all or part of your investment. When determining whether to buy our common stock, you should also refer to the other information in this prospectus,

including our consolidated financial statements and the related notes.

Risks related to our business

Our growth strategy depends on

opening new restaurants. Our ability to expand our restaurant base is influenced by factors beyond our control, which may slow restaurant development and expansion and impair our growth strategy.

We are pursuing an accelerated but disciplined growth strategy which, to be successful, will depend in large part on our ability and the

ability of our franchisees to open new restaurants and to operate these restaurants on a profitable basis. We anticipate that our new restaurants will generally take several months to reach planned operating levels due to inefficiencies typically

associated with new restaurants, including lack of market awareness, the need to hire and train sufficient team members and other factors. We cannot guarantee that we or our franchisees will be able to achieve our expansion goals or that new

restaurants will be operated profitably. Further, we cannot assure you that any restaurant we open will obtain operating results similar to those of our existing restaurants. The success of our planned expansion will depend upon numerous factors,

many of which are beyond our control, including the following:

| |

• |

|

the hiring, training and retention of qualified operating personnel, especially managers; |

| |

• |

|

reliance on the knowledge of our executives and franchisees to identify available and suitable restaurant sites; |

| |

• |

|

competition for restaurant sites; |

| |

• |

|

negotiation of favorable lease terms; |

| |

• |

|

timely development of new restaurants, including the availability of construction materials and labor; |

| |

• |

|

management of construction and development costs of new restaurants; |

| |

• |

|

securing required governmental approvals and permits in a timely manner, or at all; |

| |

• |

|

competition in our markets; and |

| |

• |

|

general economic conditions. |

Our

success depends on our ability to locate and secure a sufficient number of suitable new restaurant sites.

One

of our biggest challenges in meeting our growth objectives will be to locate and secure an adequate supply of suitable new restaurant sites. There can be no assurance that we will be able to find sufficient suitable locations, or suitable leases,

for our planned expansion in any future period. We have experienced delays in opening some of our restaurants and may experience delays in the future. Delays or failures in opening new restaurants could materially adversely affect our planned

growth.

7

Our restaurant expansion strategy focuses primarily on further penetrating existing markets. This strategy

could cause sales in some of our existing restaurants to decline.

Our areas of highest concentration are

California, Colorado, Washington and Oregon. In accordance with our expansion strategy, we intend to open new restaurants primarily in our existing markets. Because we typically draw guests from a relatively small radius around each of our

restaurants, the sales performance and guest counts for restaurants near the area in which a new restaurant opens may decline due to the opening of new restaurants.

Our expansion into new markets may present increased risks due to our unfamiliarity with the area.

Some of our new restaurants will be located in areas where we have little or no meaningful experience. Those markets may have different competitive conditions, consumer tastes and discretionary spending patterns than our

existing markets, which may cause our new restaurants to be less successful than restaurants in our existing markets. An additional risk in expansion into new markets is the lack of market awareness of the Red Robin brand. Restaurants opened in new

markets typically open at lower average weekly sales volumes than do restaurants opened in existing markets, initially resulting in higher restaurant-level operating expense ratios than in existing markets. Sales at restaurants opened in new markets

may take longer to reach average annual company-owned restaurant sales, if at all, thereby affecting the profitability of these restaurants.

Our expansion may strain our infrastructure and other resources, which could slow our restaurant development or cause other problems.

We face the risk that our existing systems and procedures, restaurant management systems, financial controls, information systems, management resources and human resources will be inadequate to support

our planned expansion of company-owned and franchised restaurants. We may not be able to respond on a timely basis to all of the changing demands that our planned expansion will impose on our infrastructure and other resources. If we fail to

continue to improve our infrastructure or to manage other factors necessary for us to achieve our expansion objectives, our operating results could be materially negatively affected.

Our ability to raise capital in the future may be limited, which could adversely impact our business.

Changes in our operating plans, acceleration of our expansion plans, lower than anticipated sales, increased expenses or other events, including those described in this section, may cause us to need to

seek additional debt or equity financing on an accelerated basis. Financing may not be available on acceptable terms, or at all, and our failure to raise capital when needed could negatively impact our growth and other plans as well as our financial

condition and results of operations. Additional equity financing may be dilutive to the holders of our common stock and debt financing, if available, may involve significant cash payment obligations and covenants and/or financial ratios that

restrict our ability to operate our business. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

If our franchisees cannot develop or finance new restaurants or build them on suitable sites or open them on schedule, our growth and success may be impeded.

Under our current form of area development agreement, franchisees must develop a predetermined number of restaurants in their area

according to a schedule that lasts for the term of their development agreement. Franchisees may not have access to the financial or management resources that they need to open the restaurants required by their development schedules, or be able to

find suitable sites on which to develop them. Franchisees may not be able to negotiate acceptable lease or purchase terms for the sites, obtain the necessary permits and government approvals or meet construction schedules. In the past, we have

agreed to extend or modify development schedules for certain areas developers, and we may do so in the future. Any of these problems could slow our growth and reduce our franchise revenues.

8

Additionally, our franchisees depend upon financing from banks and other

financial institutions in order to construct and open new restaurants. Over the past several years, financing has been difficult for small operators to obtain. Should these conditions continue into the future, the lack of adequate availability of

debt financing could adversely affect the number and rate of new restaurant openings by our franchisees and adversely affect our future franchise revenues.

Our franchisees could take actions that could harm our business.

Franchisees are

independent contractors and are not our employees. We provide training and support to franchisees, but the quality of franchised restaurant operations may be diminished by any number of factors beyond our control. Consequently, franchisees may not

successfully operate restaurants in a manner consistent with our standards and requirements, or may not hire and train qualified managers and other restaurant personnel. If franchisees do not, our image and reputation, and the image and reputation

of other franchisees, may suffer materially and system-wide sales could significantly decline.

The acquisition of existing restaurants

from our franchisees may have unanticipated consequences that could harm our business and financial condition.

We may seek to selectively acquire existing restaurants from our franchisees. To do so, we would need to identify suitable acquisition candidates, negotiate acceptable acquisition terms and obtain appropriate financing. Any

acquisition that we pursue, whether or not successfully completed, may involve risks, including:

| |

• |

|

material adverse effects on our operating results, particularly in the fiscal quarters immediately following the acquisition as it is integrated into our

operations; |

| |

• |

|

risks associated with entering into markets or conducting operations where we have no or limited prior experience; and |

| |

• |

|

the diversion of management’s attention from other business concerns. |

Future acquisitions of existing restaurants from our franchisees, which may be accomplished through a cash purchase transaction or the issuance of our equity securities, or

a combination of both, could result in potentially dilutive issuances of our equity securities, the incurrence of debt and contingent liabilities and impairment charges related to goodwill and other intangible assets, any of which could harm our

business and financial condition.

Our operations are susceptible to changes in food availability and costs which could adversely affect our

operating results.

Our profitability depends in part on our ability to anticipate and react to changes in

food costs. We rely on SYSCO Corporation, a national food distributor, as the primary supplier of our food. Any increase in distribution prices or failure to perform by SYSCO could cause our food costs to increase. There also could be a significant

short-term disruption in our supply chain if SYSCO failed to meet our distribution requirements or our relationship was terminated at the end of the contract term on June 30, 2004 or earlier by SYSCO upon breach or material deterioration of our

financial position. Further, various factors beyond our control, including adverse weather conditions, governmental regulation, production, availability and seasonality may affect our food costs or cause a disruption in our supply chain. Chicken

represented approximately 19.6% and beef represented approximately 10.0% of our food purchases in 2001. We enter into annual contracts with our beef and chicken suppliers. Our contracts for chicken are fixed price contracts. Our contracts for beef

are generally based on current market prices plus a processing fee. Changes in the price or availability of chicken or beef could materially adversely affect our profitability. We cannot predict whether we will be able to anticipate and react to

changing food costs by adjusting our purchasing practices and menu prices, and a failure to do so could adversely affect our operating results. In addition, because we provide a “value-priced” product, we may not be able to pass along

price increases to our guests.

9

Our quarterly operating results may fluctuate significantly and could fall below the expectations of securities

analysts and investors due to seasonality and other factors, resulting in a decline in our stock price.

Our

quarterly operating results may fluctuate significantly because of several factors, including:

| |

• |

|

the timing of new restaurant openings and related expenses; |

| |

• |

|

restaurant operating costs and pre-opening costs for our newly-opened restaurants, which are often materially greater during the first several months of

operation than thereafter; |

| |

• |

|

labor availability and costs for hourly and management personnel; |

| |

• |

|

profitability of our restaurants, especially in new markets; |

| |

• |

|

franchise development costs; |

| |

• |

|

increases and decreases in comparable restaurant sales; |

| |

• |

|

impairment of long-lived assets, including goodwill, and any loss on restaurant closures; |

| |

• |

|

general economic conditions; |

| |

• |

|

changes in consumer preferences and competitive conditions; and |

| |

• |

|

fluctuations in commodity prices. |

Our business is also subject to seasonal fluctuations. Historically, sales in most of our restaurants have been higher during the summer months and winter holiday season of each fiscal year. As a

result, our quarterly and annual operating results and comparable restaurant sales may fluctuate significantly as a result of seasonality and the factors discussed above. Accordingly, results for any one quarter are not necessarily indicative of

results to be expected for any other quarter or for any year and comparable restaurant sales for any particular future period may decrease. In the future, operating results may fall below the expectations of securities analysts and investors. In

that event, the price of our common stock would likely decrease.

A decline in visitors to any of the retail centers, big box shopping centers

or entertainment centers near the locations of our restaurants could negatively affect our restaurant sales.

Our restaurants are primarily located near high activity areas such as retail centers, big box shopping centers and entertainment centers. We depend on high visitor rates at these centers to attract guests to our restaurants. If

visitors to these centers decline due to economic conditions, changes in consumer preferences or shopping patterns, changes in discretionary consumer spending or otherwise, our restaurant sales could decline significantly and adversely affect our

results of operations.

If we lose the services of any of our key management personnel, our business could suffer.

Our future success significantly depends on the continued services and performance of our key management personnel, particularly Mike

Snyder, our chief executive officer and president; Jim McCloskey, our chief financial officer; Mike Woods, our senior vice president of franchise development; Bob Merullo, our senior vice president of restaurant operations; Todd Brighton, our vice

president of development; and Eric Houseman, our vice president of restaurant operations. Our future performance will depend on our ability to motivate and retain these and other executive officers and key team members, particularly regional

operations directors, restaurant general managers and kitchen managers. Competition for these employees is intense. The loss of the services of members of our senior management or key team members or the inability to attract additional qualified

personnel as needed could materially harm our business.

10

Approximately 83.3% of our company-owned restaurants are located in the Western United States and, as a result,

we are sensitive to economic and other trends and developments in this region.

We currently operate a total

of 75 company-owned restaurants in the Western United States. As a result, we are particularly susceptible to adverse trends and economic conditions in this region, including its labor market. In addition, given our geographic concentration,

negative publicity regarding any of our restaurants in the Western United States could have a material adverse effect on our business and operations, as could other regional occurrences such as local strikes, energy shortages or increases in energy

prices, droughts or earthquakes or other natural disasters.

Our future success depends on our ability to protect our proprietary information.

Our business prospects will depend in part on our ability to develop favorable consumer recognition of

the Red Robin name and logo. Although Red Robin®, America’s Gourmet Burgers &

Spirits® and Mad Mixology® are federally registered trademarks with the United States Patent and Trademark Office and in Canada, our trademarks could be infringed in ways

that leave us without redress, such as by imitation. In addition, we rely on trade secrets and proprietary know-how, and we employ various methods, to protect our concepts and recipes. However, such methods may not afford adequate protection and

others could independently develop similar know-how or obtain access to our know-how, concepts and recipes. Moreover, we may face claim(s) of infringement that could interfere with our use of our proprietary know-how, concepts, recipes or trade

secrets. Defending against such claim(s) may be costly and, if we are unsuccessful, we may be prevented from continuing to use such proprietary information in the future and/or be forced to pay damages. We do not maintain confidentiality and

non-competition agreements with all of our executives, key personnel or suppliers. In the event competitors independently develop or otherwise obtain access to our know-how, concepts, recipes or trade secrets, the appeal of our restaurants could be

reduced and our business could be harmed. We franchise our system to various franchisees. While we try to ensure that the quality of our brand and compliance with our operating standards, and the confidentiality thereof are maintained by all of our

franchisees, we cannot assure that our franchisees will avoid actions that adversely affect the reputation of Red Robin or the value of our proprietary information.

Risks related to the food service industry

Changes in consumer preferences or discretionary consumer spending could negatively impact our results of operations.

Our restaurants feature burgers, salads, soups, appetizers, other entrees such as rice bowls and pasta, desserts and our signature Mad Mixology® alcoholic and non-alcoholic beverages in a family-friendly atmosphere. Our continued success depends, in part,

upon the popularity of these foods and this style of casual dining. Shifts in consumer preferences away from this cuisine or dining style could materially adversely affect our future profitability. The restaurant industry is characterized by the

continual introduction of new concepts and is subject to rapidly changing consumer preferences, tastes and eating and purchasing habits. While burger consumption in the United States has grown over the past 20 years, the demand may not continue to

grow or taste trends may change. Our success will depend in part on our ability to anticipate and respond to changing consumer preferences, tastes and eating and purchasing habits, as well as other factors affecting the food service industry,

including new market entrants and demographic changes. Also, our success depends to a significant extent on numerous factors affecting discretionary consumer spending, including economic conditions, disposable consumer income and consumer

confidence. Adverse changes in these factors could reduce guest traffic or impose practical limits on pricing, either of which could harm our results of operations.

11

Health concerns relating to the consumption of beef or other food products could affect consumer preferences

and could negatively impact our results of operations.

Like other restaurant chains, consumer preferences

could be affected by health concerns about the consumption of beef, the key ingredient in many of our menu items, or negative publicity concerning food quality, illness and injury generally, such as negative publicity concerning e-coli, “mad

cow” or “foot-and-mouth” disease, publication of government or industry findings concerning food products served by us, or other health concerns or operating issues stemming from one restaurant or a limited number of restaurants. This

negative publicity may adversely affect demand for our food and could result in a decrease in guest traffic to our restaurants. If we react to the negative publicity by changing our concept or our menu, we may lose guests who do not prefer the new

concept or menu, and may not be able to attract a sufficient new guest base to produce the revenue needed to make our restaurants profitable. In addition, we may have different or additional competitors for our intended guests as a result of a

concept change and may not be able to compete successfully against those competitors. A decrease in guest traffic to our restaurants as a result of these health concerns or negative publicity or as a result of a change in our menu or concept could

materially harm our business.

Labor shortages could slow our growth or harm our business.

Our success depends in part upon our ability to attract, motivate and retain a sufficient number of qualified, high energy team members.

Qualified individuals of the requisite caliber and number needed to fill these positions are in short supply in some areas. The inability to recruit and retain these individuals may delay the planned openings of new restaurants or result in high

employee turnover in existing restaurants, which could harm our business. Additionally, competition for qualified team members could require us to pay higher wages to attract sufficient team members, which could result in higher labor costs. Most of

our employees are paid in accordance with minimum wage regulations. Accordingly, any increase, whether state or federal, could have a material adverse impact on our business.

We are subject to extensive government laws and regulations that govern various aspects of our business. Our operations and our ability to expand and develop our restaurants may be adversely affected by these

laws and regulations, which could cause our revenues to decline and adversely affect our growth strategy.

The

restaurant industry is subject to various federal, state and local government regulations, including those relating to the sale of food and alcoholic beverages. While at this time we have been able to obtain and maintain the necessary governmental

licenses, permits and approvals, the failure to maintain these licenses, permits and approvals, including food and liquor licenses, could adversely affect our operating results. Difficulties or failure in obtaining the required licenses and

approvals could delay or result in our decision to cancel the opening of new restaurants. Local authorities may suspend or deny renewal of our food and liquor licenses if they determine that our conduct does not meet applicable standards or if there

are changes in regulations.

We are subject to “dram shop” statutes in some states. These statutes

generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. A judgment substantially in excess of our insurance coverage could harm our

financial condition.

Various federal and state labor laws govern our relationship with our employees and affect

operating costs. These laws include minimum wage requirements, overtime pay, unemployment tax rates, workers’ compensation rates, citizenship requirements and sales taxes. Additional government-imposed increases in minimum wages, overtime pay,

paid leaves of absence and mandated health benefits, increased tax reporting and tax payment requirements for employees who receive gratuities, or a reduction in the number of states that allow tips to be credited toward minimum wage requirements

could harm our operating results.

The Federal Americans with Disabilities Act prohibits discrimination on the

basis of disability in public accommodations and employment. Although our restaurants are designed to be accessible to the disabled, we could be required to make modifications to our restaurants to provide service to, or make reasonable

accommodations for, disabled persons.

12

We are also subject to federal regulation and state laws that regulate the offer

and sale of franchises and aspects of the licensor-licensee relationship. Many state franchise laws impose restrictions on the franchise agreement, including limitations on non-competition provisions and the termination or non-renewal of a

franchise. Some states require that franchise materials be registered before franchises can be offered or sold in the state.

A significant

increase in litigation could have a material adverse effect on our results of operations, financial condition and business prospects.

As a participant in the restaurant industry, we are sometimes the subject of complaints or litigation from guests alleging illness, injury or other food quality, health or operational concerns. Adverse publicity resulting

from these allegations could harm our restaurants, regardless of whether the allegations are valid or whether we are liable. In fact, we are subject to the same risks of adverse publicity resulting from these sorts of allegations even if the claim

actually involves one of our franchisees. Further, employee claims against us based on, among other things, discrimination, harassment or wrongful termination may divert our financial and management resources that would otherwise be used to benefit

the future performance of our operations.

Our success depends on our ability to compete effectively in the restaurant industry.

Competition in the restaurant industry is increasingly intense. We compete on the basis of the taste,

quality, and price of food offered, guest service, ambiance and overall dining experience. We believe that our operating concept, attractive dining value and quality of food and guest service, enable us to differentiate ourselves from our

competitors. Our competitors include a large and diverse group of restaurant chains and individual restaurants that range from independent local operators that have opened restaurants in various markets, to well-capitalized national restaurant

companies. In addition, we compete with other restaurants and with retail establishments for real estate. Many of our competitors are well-established in the casual dining market segment and some of our competitors have substantially greater

financial, marketing and other resources than do we.

Risks

related to this offering

Our stock price may be volatile, and you may not be able

to resell your shares at or above the initial offering price.

Prior to this offering, there has been no

public market for shares of our common stock. An active trading market may not develop or be sustained following completion of this offering. The initial public offering price of the shares has been determined by negotiations between us and

representatives of the underwriters. The price may bear no relationship to the price at which our common stock will trade upon completion of this offering. The stock market has experienced significant price and volume fluctuations. Fluctuations or

decreases in the trading price of our common stock may adversely affect your ability to trade your shares.

In the

past, following periods of volatility in the market price of a company’s securities, securities class action litigation has often been instituted. A securities class action suit against us could result in substantial costs and divert

management’s attention and resources that would otherwise be used to benefit the future performance of our operations.

Approximately 66.5%

of our outstanding shares of common stock may be sold into the public market in the future, which could depress our stock price.

The 5,038,000 shares of common stock sold in this offering (and any shares sold upon exercise of the underwriters’ over-allotment option) will be freely tradable without restriction under the Securities Act of 1933,

except for any shares held by our officers, directors and principal stockholders. After this offering, approximately an additional 614,927 shares of common stock will be freely tradable under Rule 144(k) under the Securities Act, unless any of such

shares are purchased by one of our existing affiliates as that term is defined in Rule 144 under the Securities Act.

13

After this offering, approximately 9,372,727 shares of our common stock which

are outstanding and held by our affiliates will be subject to the volume and other limitations of Rule 144 or Rule 701 under the Securities Act. Our directors, officers and a significant number of our stockholders, who together will own a majority

of the shares of our common stock outstanding after this offering, have entered or will enter into lock-up agreements prior to the consummation of this offering under which the holders have agreed or will agree not to sell or otherwise dispose of

any of their shares for a period of 180 days after the date of this prospectus without the prior written consent of Banc of America Securities LLC. In its sole discretion and at any time without notice, Banc of America Securities LLC may release all

or any portion of the shares subject to the lock-up agreements. All of the shares subject to lock-up agreements will become available for sale in the public market immediately following expiration of the 180 day lock-up period, subject (to the

extent applicable) to the volume and other limitations of Rule 144 or Rule 701 under the Securities Act. After expiration of the lock-up period, some of our stockholders have the contractual right to require us to register 9,679,435 shares of common

stock for future sale.

In addition, following this offering, we intend to file registration statements

under the Securities Act registering an aggregate of 1,980,156 shares under our option plans and up to 300,000 shares under employee stock purchase plan. Shares included in such registration statements will be available for sale in the public market

immediately after the 180-day lock-up period expires.

Sales of substantial amounts of common stock in the

public market, or the perception that these sales may occur, could adversely affect the prevailing market price of our common stock and our ability to raise capital through a public offering of our equity securities. See “Shares Eligible for

Future Sale” which describes the circumstances under which restricted shares or shares held by affiliates may be sold in the public market.

Some of our stockholders could exert significant influence or control over us, and may not make decisions that are in the best interests of all stockholders.

After this offering, Quad-C, through its affiliates, will own approximately 28.7% of our outstanding common stock, Skylark Co., Ltd., through its affiliates, will own

approximately 15.7% of our outstanding common stock, Mike Snyder will own approximately 9.9% of our outstanding common stock, and our officers, directors and principal stockholders, i.e., stockholders holding more than 5.0% of our common stock,

including Quad-C, Skylark and Mike Snyder, will together hold approximately 58.0% of our outstanding common stock. See “Principal and Selling Stockholders.” These stockholders, acting individually or together, could exert significant

influence over all matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions and, acting together, could control any vote of our stockholders requiring approval of a majority of

our outstanding common stock. This concentration of ownership may delay or prevent a change in control of our company, and make some transactions more difficult or impossible without the support of these stockholders. Also, the interests of these

stockholders may not always coincide with our interests as a company or the interest of other stockholders. Accordingly, Quad-C, Skylark, Mike Snyder and these other stockholders could cause us to enter into transactions or agreements that you would

not approve. Our certificate of incorporation and bylaws require a supermajority vote of our stockholders, i.e. 66 2/3%, only to remove a director or to amend our bylaws or specified provisions of our certificate of incorporation.

As

a new investor, you will experience immediate and substantial dilution in net tangible book value.

Investors

purchasing shares of our common stock in this offering will pay more for their shares than the amount paid by existing stockholders who acquired shares prior to this offering. Accordingly, if you purchase common stock in this offering, you will

incur immediate dilution in pro forma net tangible book value of approximately $10.33 per share. If the holders of outstanding options or warrants exercise these options or warrants, you will incur further dilution. See “Dilution.”

14

Provisions in Delaware law and our charter may prevent or delay a change of control, even if that change of

control may be beneficial to our stockholders.

We are subject to the Delaware anti-takeover laws regulating

corporate takeovers. These anti-takeover laws prevent Delaware corporations from engaging in business combinations with any stockholder, including all affiliates and associates of the stockholder, who owns 15.0% or more of the corporations’

outstanding voting stock, for three years following the date that the stockholder acquired 15.0% or more of the corporation’s voting stock unless specified conditions are met, as further described in “Description of Capital Stock.”

Prior to the consummation of this offering, we intend to amend and restate our certificate of incorporation and

bylaws. Our amended and restated certificate of incorporation and bylaws will include a number of provisions that may deter or impede hostile takeovers or changes of control of management. These provisions will:

| |

• |

|

authorize our board of directors to establish one or more series of preferred stock, the terms of which can be determined by the board of directors at the time

of issuance; |

| |

• |

|

divide our board of directors into three classes of directors, with each class serving a staggered three-year term. As the classification of the board of

directors generally increases the difficulty of replacing a majority of the directors, it may tend to discourage a third party from making a tender offer or otherwise attempting to obtain control of us and may maintain the composition of the board

of directors; |

| |

• |

|

not provide for cumulative voting in the election of directors unless required by applicable law. Under cumulative voting, a minority stockholder holding a

sufficient percentage of a class of shares may be able to ensure the election of one or more directors; |

| |

• |

|

provide that a director may be removed from our board of directors only for cause, and then only by a supermajority vote of the outstanding shares;

|

| |

• |

|

require that any action required or permitted to be taken by our stockholders must be effected at a duly called annual or special meeting of stockholders and

may not be effected by any consent in writing; |

| |

• |

|

state that special meetings of our stockholders may be called only by the chairman of the board of directors, our chief executive officer, by the board of

directors after a resolution is adopted by a majority of the total number of authorized directors, or by the holders of not less than 10.0% of our outstanding voting stock; |

| |

• |

|

provide that the chairman or other person presiding over any stockholder meeting may adjourn the meeting whether or not a quorum is present at the meeting;

|

| |

• |

|

establish advance notice requirements for submitting nominations for election to the board of directors and for proposing matters that can be acted upon by

stockholders at a meeting; |

| |

• |

|

provide that certain provisions of our certificate of incorporation can be amended only by supermajority vote of the outstanding shares, and that our bylaws can

be amended only by supermajority vote of the outstanding shares or our board of directors; |

| |

• |

|

allow our directors, not our stockholders, to fill vacancies on our board of directors; and |

| |

• |

|

provide that the authorized number of directors may be changed only by resolution of the board of directors. |

Your ability to seek potential recoveries from Arthur Andersen LLP with respect to claims arising from its work on The Snyder Group Company financial statements may

be significantly limited.

Investors’ ability to seek potential recoveries from Arthur Andersen

LLP related to any claim such investors may assert as a result of the work performed by Arthur Andersen on The Snyder Group Company financial statements included in this prospectus may be significantly limited.

15

This prospectus contains forward-looking statements. These

statements relate to future events or our future financial performance. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,”

“could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should” or “will” or the negative of these terms or other

comparable terminology.

These statements are only predictions and involve known and unknown risks, uncertainties

and other factors, including those relating to:

| |

Ÿ |

|

our ability to achieve and manage our planned expansion; |

| |

Ÿ |

|

our ability to raise capital in the future; |

| |

Ÿ |

|

the ability of our franchisees to open and manage new restaurants; |

| |

Ÿ |

|

our franchisees’ adherence to our practices, policies and procedures; |

| |

Ÿ |

|

changes in the availability and costs of food; |

| |

Ÿ |

|

potential fluctuation in our quarterly operating results due to seasonality and other factors; |

| |

Ÿ |

|

the continued service of key management personnel; |

| |

Ÿ |

|

the concentration of our restaurants in the Western United States; |

| |

Ÿ |

|

our ability to protect our name and logo and other proprietary information; |

| |

Ÿ |

|

changes in consumer preferences or consumer discretionary spending; |

| |

Ÿ |

|

health concerns about our food products; |

| |

Ÿ |

|

our ability to attract, motivate and retain qualified team members; |

| |

Ÿ |

|

the impact of federal, state or local government regulations relating to our team members or the sale of food and alcoholic beverages;

|

| |

Ÿ |

|

the impact of litigation; and |

| |

Ÿ |

|

the effect of competition in the restaurant industry. |

Other risks, uncertainties and factors, including those discussed under “Risk Factors,” could cause our actual results to differ materially from those projected in any forward-looking

statements we make.

We assume no obligation to publicly update or revise these forward-looking statements for any

reason, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

16

We estimate that we will receive net proceeds from the sale of

4,000,000 shares of common stock in this offering of $54.7 million, based on an assumed initial public offering price of $15.00 per share, after deducting underwriting discounts and commissions and estimated offering expenses. We will not receive

any proceeds from the sale of shares by the selling stockholders.

We intend to use the net proceeds of this

offering as follows:

| |

Ÿ |

|

approximately $47.9 million to repay the outstanding amounts under our term loan with Finova Capital Corporation, including a prepayment penalty of 4.0%, which

bears interest at 9.9% and has a maturity date of September 1, 2012. |

| |

Ÿ |

|

approximately $3.5 million to repay the outstanding amounts under our revolving credit facility with U.S. Bank National Association, which bears interest at the

London Interbank Offered Rate, or LIBOR, plus 3.0% and has a maturity date of March 31, 2003. We entered into this revolving credit facility for working capital and capital expenditure needs. |

| |

Ÿ |

|

approximately $1.6 million to repay the outstanding amounts under one real estate loan with Captec Financial Group, including a prepayment penalty of 1.0%,

which bears interest at 10.1% and has a maturity date of January 1, 2012. |

| |

Ÿ |

|

approximately $0.5 million to repay the outstanding amounts under two equipment loans with Captec and one equipment loan with General Electric Capital

Corporation, which bear interest at rates ranging from 9.6% to 11.6% and have maturity dates between April 1, 2003 and December 1, 2003. |

We intend to use the balance of the net proceeds for general corporate purposes, which may include the opening of new restaurants or the acquisition of existing restaurants from our franchisees if we

receive sufficient proceeds. We regularly consider acquisitions of existing restaurants from our franchisees in the ordinary course of business, although we currently have no agreements regarding any future acquisitions. Pending use for general

corporate purposes, opening new restaurants or making acquisitions, we intend to invest the net proceeds in short-term, investment-grade, interest-bearing securities. We cannot predict whether the proceeds invested will yield a favorable return. We